- Launch already newsletter 🚀

- Posts

- How I Became a Seven-Figure Pharmacist...

How I Became a Seven-Figure Pharmacist...

+ 5 Wealth-Building Strategies to Implement

Jamie Wilkey

July 22, 2024 • Estimated Reading Time: 11 minutes

Presented by

Issue #106

Subscriber count: 11,204+

Hi there! 👋🏻 I’m a 7-figure pharmacist. I’m guessing you want to be one too, which is a big part of why you’re interested in building your own thing. This week I wanted to talk about money with you, so I brought in my good friend and financial master, Dr. Tim Ulbrich to share how he also became a 7-figure pharmacist. In this article he shares 5 wealth-building strategies you can implement too.

First, a quick message from this week’s sponsor: 👇🏻

Why are all your favorite newsletters switching to beehiiv?

It’s because the founding beehiiv team were all early Morning Brew employees who helped scale that newsletter to over 4 million daily subscribers.

Years of trial and error went into building the precise tools, dashboards, and analytics needed to accomplish that. And now every newsletter on beehiiv has access to the same winning formula.

So what exactly does beehiiv offer?

World-class growth tools like the referral program and recommendation network

Monetization via the beehiiv Ad Network and premium subscriptions (i.e. beehiiv helps you get paid)

Seamless content creation with a sleek collaborative editor

Best-in-class inbox deliverability of 99%

Oh and it’s the most affordable by a mile…

Take your newsletter to the next level — get started for free.

How I Became a Seven-Figure Pharmacist…

And 5 Wealth-Building Strategies to Implement

In 2009, I finished my PGY1 residency (making a whopping $31,000!) and finally reached the other side, ready to cash in on the mystical six-figure pharmacist income.

Everything was looking good until I realized I overlooked one minor detail…

I was broke.

No, not “broke, broke.”

But definitely “high-earner broke.”

My wife, Jess, and I were in spectacular shape on the surface, but underneath our comfortable lifestyle and my new six-figure income, our finances told a different story.

We had over $200,000 of student loan debt.

We had a house with almost no equity.

We had very little in savings.

And soon had a growing family to support.

I realized that despite the amazing opportunities that graduating with a PharmD offers, there’s a little-discussed truth among practitioners in the field:

Most pharmacists make a good income but find themselves in exactly the same boat.

As I reflect on this journey, I am grateful for the experiences I’ve had and for what I’ve learned along the way.

I also feel fear and anxiety when acknowledging that my perception of the six-figure income and the reality of what it could do were two very different things.

The Pivot Point

It took me 4 humbling years to realize that my six-figure income wasn’t all it was cracked up to be.

One book in particular hit me across the head at just the right time.

It was a wake-up call that I needed.

The personal finance classic The Millionaire Next Door taught me that net worth, not income, indicates your financial health.

More to come on this later but for now, understand that net worth, your assets (what you own) minus your liabilities (what you owe), paints a nice picture of what did (or didn’t) happen with your income.

After reading this book I decided it was time to put pen to paper and do my calculation.

The assets column was on the left side of the paper, and the liabilities column was on the right side of the paper.

The left side was fairly blank, and the right side included a laundry list of liabilities highlighted by none other than those pesky student loans (many of which were hanging out at 6.8%).

This calculation showed that just four years after graduating from pharmacy school, we had earned nearly a half-million dollars in income but had a net worth of NEGATIVE $225,000.

Ouch.

I was overwhelmed with student loan debt.

I was confused about how to best save and invest for the future.

I was frustrated by the fact that I was making a good income but not progressing financially.

If you are like most pharmacists I talk with, your journey may include something similar.

You might even be there now.

And it wouldn’t be so frustrating if you hadn't already done everything “right.”

You got the degree.

You landed a high-paying job.

You started making “smart” decisions by buying a house, investing, getting a reliable car, and finally reaping the rewards of all your hard work.

But aside from a few Obi-Wan Kenobi-like aphorisms about getting your “financial house in order,” no one tells you that, despite the great salary, the battle is far from over.

Now, thankfully this story has a happy ending.

Because just 3 years after my wife, Jess, and I decided to get serious, stop messing around, and take control of our finances, in the fall of 2015, we submitted the very last of our student loan payments (still have the screenshot… take that Navient!).

We had to self-teach, and we made several mistakes along the way (more on this later).

No one in our sphere was talking about this.

And it was HARD, but it was worth it.

From $0 to $1 Million

When we hit submit on that last student loan payment, it sure felt like we had arrived…finally.

That would be the first of many times we would learn the important lesson that there is no such thing as arrived when it comes to the financial plan.

There’s always an opportunity to grow and learn.

Once we had crossed the line from a negative net worth to $0, it was go time.

Finally, we could play offense.

And through methodical savings, investing, diligent spending, planning, and working our butt off building a business, we would eventually cross a net worth of $1M in late 2020.

That’s right.

Negative $225,000 in 2012 to $1M+ in approximately 8 years.

I want pharmacists like yourself to be fully armed and empowered with the knowledge and tools needed to live a rich life today and tomorrow.

You can get there.

But in addition to your income, you need the right mindset, strategy, and habits to achieve success.

It can be done.

Here’s what I’m excited to share with you.

It’s not complicated.

It doesn’t include fancy spreadsheets and nuanced investment vehicles.

It doesn’t take an exorbitant amount of time.

It doesn’t mean you have to live on rice and beans.

I did it, and you can do it too.

What Does Success Look Like?

I recently had a group of pharmacists reflect on a question that helped them clarify what matters most to them in their lives and how their financial plans can support those areas.

Here are just a few of the responses:

"Travel the world - give generously - fund kids’ hopes"

"Take my kids to see the world"

"Have a home with space and time to host family and friends often"

"Volunteer locally, spend time with family, and learn new skills"

"Open my own business"

"Working part-time without the fear of finances would allow me to volunteer more and do something more passionate."

"Create a community center for people who use drugs to help provide basic social needs and treatment (addiction is my specialty area)"

Yes, yes, yes!!

Notice what you don't see written here.

You don't see people talking about having a pristine zero-based budget.

You don't see people discussing having a certain amount of money in the bank.

You don't see people talking about having a complicated, time-intensive investing strategy.

You don’t see comments about having a 4.6% high-yield savings account over a 4.2% savings account.

You don’t see any comments about PSLF optimization.

While there's nothing wrong with any one of these things (I myself like a nice budget!), it's important we remember that these things aren't the end goals and determinants of success but rather steps along the way to support living a rich life today and tomorrow.

So before you go all Type-A pharmacist on me and start making moves, getting a dopamine hit, and checking things off the list, take a step back and ask yourself these questions.

What am I trying to accomplish?

What’s the purpose?

What does success look like?

After all, money is a tool for living a rich life.

It’s up to you to decide what that rich life looks like.

5 Wealth-Building Strategies to Implement

Ok, it’s time to take action.

Here are 5 wealth-building strategies you can employ right now.

None of that fluffy impractical stuff.

I’ve implemented all of these in my plan.

Step #1 - Track Your Net Worth

I told you we’d be coming back to this.

In The Millionaire Next Door, Tom Stanley says, "One of the reasons that millionaires are economically successful is that they think differently."

What he is referring to, in part, is that those who build wealth realize that income is not the metric of success but rather a tool for building wealth.

It’s worth repeating what I wrote before.

Net worth (what you own - what you owe), not income, is the true indicator of your financial health.

Understanding and respecting this calculation can propel your financial plan.

Discovering net worth was a mindset shift and pivot point for our journey.

We update this net worth tracking sheet once a month, which allows us to take a step back and see the overall trajectory and bigger picture while focusing on our short-term goals.

To access this spreadsheet template and other resources mentioned in this article, view My Toolbox and make a copy of the resources that you can use in your planning.

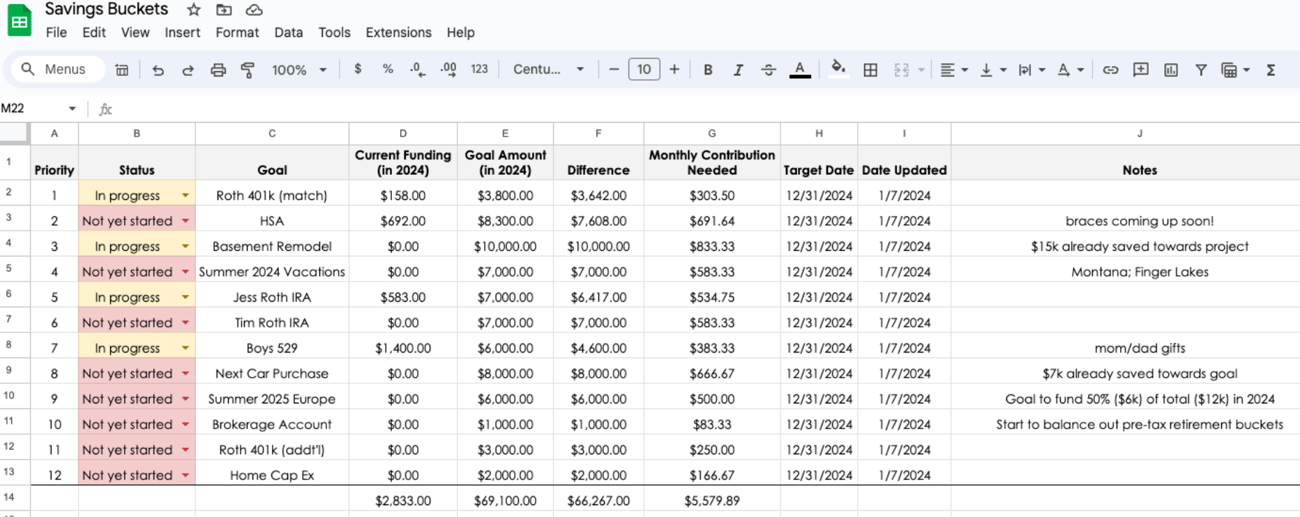

#2 - Set Up Savings Buckets

Once Jess and I are on the same page with the goals for the year, it's time to write them down and prioritize accordingly so we can start to implement a plan to achieve them.

Otherwise, it’s a hope, wish, or dream.

For each goal, we define the following:

Amount needed to achieve the goal

The current amount saved toward the goal

The gap between the amount needed and the amount saved

The monthly contribution needed to close the gap

Here's a look at our 2024 savings bucket sheet:

From here, we can work the budget to determine how much is available each month to allocate towards the goals and make any necessary adjustments.

Then, we can set up buckets (we use Ally, but you can do something similar on your own or perhaps with your bank) to have a bucket for each goal (except those that go directly to outside accounts such as IRAs, HSA, and 529s).

This is where things get real...moving away from "we hope..." and "we wish..."

If this looks complicated, don’t let it fool you.

The bucket system we set up took about 15 minutes because the hard work was already done in the goal-setting and prioritization process.

#3 - Create a Legacy Folder

While a legacy folder isn’t going to directly move the needle on your net worth, don’t underestimate what it can offer in terms of peace of mind knowing that, in the event of an emergency, all of your financial documents are organized and in one location.

Think of the "legacy folder" as a one-stop shop where you have all of your important financial information, records, and systems such that, if someone else had access, they could quickly pick up where you left off.

Our legacy folder is a combination of a shared Google Drive and a fireproof safe at home.

Our financial planning team has shared access as well our family who would be caring for our boys in the event something happened to us. All passwords are stored separately using 1Password

Access My Toolbox for a ‘Legacy Folder Table of Contents’.

#4 - Up Your Financial IQ

“How much do I need to save to retire?”

“How can I best save and invest for the future?”

“What should my asset allocation be?”

“Do I need a life or disability insurance policy?”

“How can I optimize student loan or other debt repayment?”

“Should I save and invest or pay down debt?”

Sound familiar?

This is real-life stuff.

If any of these hit home, know that you aren't alone.

Reflecting on my journey, I realize that knowledge (along with community and accountability) was a key missing ingredient.

Despite being a personal finance nerd today, my financial IQ was limited at the time.

When I was finishing up my PharmD training, I couldn't tell you the difference between a 401(k) and an IRA, a stock versus a bond, secured versus unsecured debt, unsubsidized versus subsidized loans, a tax credit versus deduction—the list goes on.

My ignorance led to mistakes and delays in our progress.

My lack of financial IQ wasn't my fault.

If you feel similarly, know it's not your fault either.

Our K-12 system does an atrocious job of prioritizing financial literacy.

While I'm grateful for my AP Calculus class and how that saved me from having to take a semester of Calculus in college, I use very little calculus in my life today.

Contrast that with personal finance, which I use in some form or fashion daily.

So why do we invest so little time in financial literacy, knowing that its application will be wide for everyone?

Great question.

It's a tragedy but one we have to overcome.

While the lack of financial education we received during K-12 isn't our fault, it is our fault if we don't take action now, knowing that we can learn just about anything we want.

The good news is we can overcome it if we are willing to invest some time and energy.

Not an AP course-level type of time...just a little bit of time invested will yield HUGE benefits.

Shameless plug! If you aren’t already listening to the Your Financial Pharmacist Podcast, check it out. It will level up your financial IQ. We publish new episodes every Thursday and have a library of 350+ episodes covering various topics.

#5 - Respect the Power of Compound Interest & Time Value of Money

If you aren’t in awe of the time value of money, you haven’t spent enough time nerding out on savings calculators.

“Compound interest is the eighth wonder of the world. He who understands it, earns it…he who doesn’t…pays it.”

Albert Einstein is credited with this quote that should peak our curiosity about the power of investing.

More specifically, the power of compound interest.

It's one of those financial jargon terms we throw around that we know is important but may not be sure what it means and why it matters.

Compound interest is the process by which an investment grows exponentially over time because both the original investment and interest gained earn interest over time.

Let’s break it down.

For example, if you were to invest $1,000 today and earn an average of 10% per year in growth (interest), you would have $1,100 after year 1 ($1,000 x 1.1).

An important side note before we go any further. I’m NOT suggesting you should expect a clean 10% rate of return every year. Investments don't work that way and it's a simple calculation to show how compound interest works.

At the end of year 2, you would earn an additional 10% on the original investment ($1,000) plus the interest earned in year one ($100).

Therefore, you would have $1,210 after year 2 ($1,100 x 1.1).

Fast-forward 30 years and your original investment of $1,000 is worth approximately $20,000!

If you were to use much bigger numbers (as will be the case with your retirement savings) over a long period of time, you can really appreciate the snowball effect of compound interest.

Through the power of compound interest over a long period of time, we can see how investing has the potential to yield a passive income stream.

And if we’re playing our cards right, there should be a point in the future when interest earned on investments is out-earning our income.

Now we’re talking.

Using a simple compound interest calculator, we can see that if someone starts with $100,000 of savings, adds $100/month over 25 years, and the portfolio grows, on average, 7% per year, they will have saved $618,642 dollars at the end of the 25 year time period.

What if, instead, they could save $500 per month?

The balance of the account is estimated to be $922,237.

How about $1,000 per month?

$1,301,732.

And here’s the kicker.

Of the $1.3 million, over 70% will be from interest earned.

That’s the power of compound interest.

As the numbers highlight, the earlier we save and the more aggressively we save (in the form of the monthly contribution amount), the more magical compound interest seems and the faster the path to creating a passive income stream.

It’s Your Turn

As you start to implement your plan, let me offer two words of encouragement.

First, avoid analysis paralysis by identifying the one next move you can make.

This is a marathon, not a sprint.

As Lao Tzu said, “The journey of a thousand miles begins with a single step.”

One step after another over a long period of time will yield results.

That’s what Darren Hardy refers to in his book The Compound Effect when he says, “Small, Smart Choices + Consistency + Time = Radical Difference.”

Second, your journey will inevitably include mistakes.

Trust me, I’ve made my fair share.

Here are just a few:

Paying too much student loan debt (my financial IQ on loan forgiveness and refinancing was lacking)

Buying a home too early

Delaying the purchase of term-life insurance with young children

Delaying the establishment of estate planning docs

Cashing out pre-tax retirement funds

Buying a car I had no business buying

Since mistakes will happen, we must learn to give ourselves some grace.

You got this, and I’m here cheering you on.

—

A big THANK YOU to Dr. Jamie Wilkey for allowing me the space to share my story and provide tips to help you build wealth and find the balance between saving for the future and living a rich life today.

If you would like to learn more about Your Financial Pharmacist, you can visit www.yourfinancialpharmacist.com/. Furthermore, to get financial tips delivered to your inbox each week, you can sign up for the YFP Money Matters newsletter at www.yourfinancialpharmacist.com/newsletter

Onward!

-Tim Ulbrich, PharmD

I hope you enjoyed this week’s issue all about money. I know I did. I’ve followed the principles Tim has shared above and I’m thoroughly enjoy being a 7-figure PharmD who just turned 38 years old this year.

👋🏻 Jamie

PS-Whenever you're ready, there are 2 more ways Jamie can help you:

I'm building a waitlist for my private community of PharmDs building their own thing online. This group will turn your expertise into influence and your silence into success. Join here 👈🏻

Hit reply to this email with a problem you’re facing:

- starting/growing your digital business

- or getting out of a traditional pharmacist job

Chances are I’ll write a newsletter to solve your problem if it applies to others. 😉